Credit card fraud protection in India 2026 has never been more critical — and India’s digital payment revolution has a dark side.

With over 170 million credit card details exposed globally in 2025 — a staggering 186% surge in breached records — and credit card fraud cases rising 29.5% year-on-year in India, protecting your plastic has never been more urgent.

The good news? The Reserve Bank of India (RBI) is fighting back with landmark rules in 2026 that shift more power into your hands.

This comprehensive guide covers everything — from the latest RBI credit card fraud rules 2026, to actionable credit card protection tips India users can apply today.

What Is Credit Card Fraud? (And Why India Is a Target)

Credit card fraud occurs when someone uses your credit card details — without your authorization — to make purchases, withdraw cash, or conduct financial transactions.

India is particularly vulnerable because of its explosive digital payment adoption combined with varying levels of financial literacy across demographics.

Credit card fraud accounts for 7% of all digital fraud cases in India as of 2026, and the numbers are accelerating.

The most alarming statistic: card-not-present (CNP) fraud rate stands at 0.93%, which is nearly 90 times higher than in-person fraud (0.06%).

This means online credit card transactions — shopping, bill payments, subscriptions — carry the highest risk for Indian cardholders.

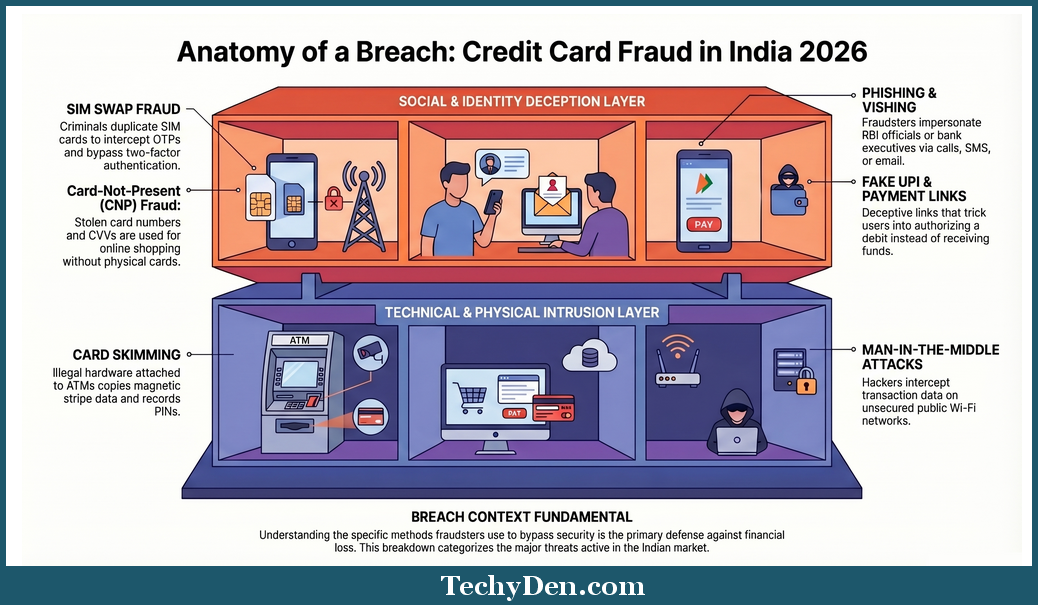

Types of Credit Card Fraud in India 2026

Understanding how fraudsters operate is your first line of defense. Here are the most common credit card scams in India active right now:

1. Phishing & Vishing Attacks

Fraudsters impersonate your bank via SMS, email, or phone calls, asking you to “verify” your card details, OTP, or CVV. Vishing (voice phishing) has surged in India, with callers posing as RBI officials or bank executives.

2. SIM Swap Fraud

This is one of the most dangerous credit card scams in India in 2026. Criminals convince your telecom provider to issue a duplicate SIM card. Once they control your phone number, they intercept all OTPs and bypass two-factor authentication — emptying your account within minutes.

3. Card Skimming at ATMs

Illegal skimming devices are attached to ATM card slots or PoS terminals to copy your card’s magnetic stripe data. Combined with a hidden camera capturing your PIN, fraudsters create cloned cards and withdraw cash.

4. Card-Not-Present (CNP) Fraud

The most prevalent form of online credit card fraud in India. Your 16-digit card number, expiry date, and CVV are stolen — often through data breaches or dark web purchases — and used for online shopping without the physical card.

5. Man-in-the-Middle Attacks

Hackers intercept data between your browser and a payment gateway, especially on unsecured public Wi-Fi networks. This is why using a VPN for credit card safety in India is increasingly recommended.

6. Fake UPI & Payment Link Scams

Fraudsters send fake payment request links claiming to “send” you money. Accepting the request actually debits your account. This hybrid UPI-credit card fraud is uniquely prevalent in India.

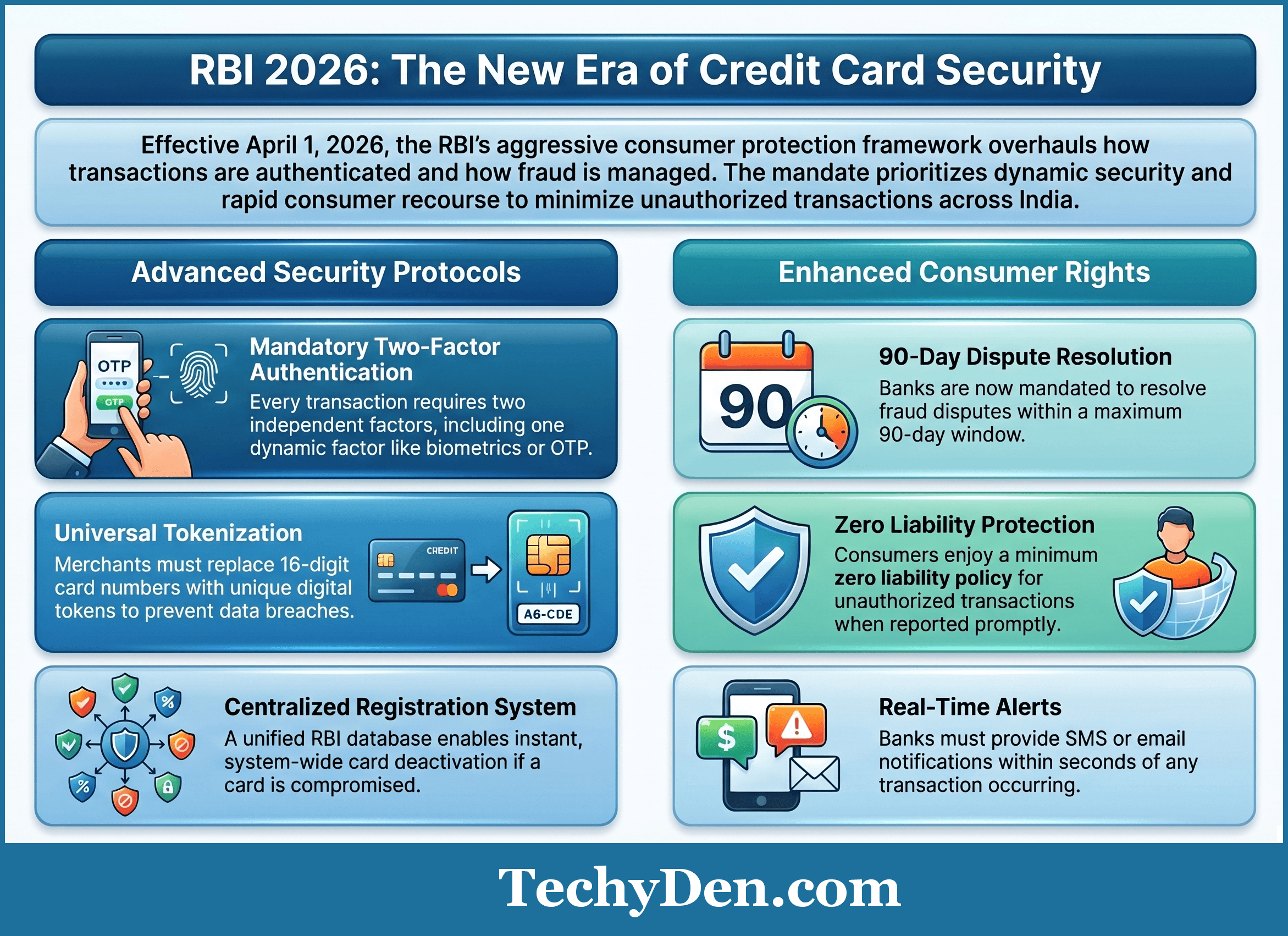

RBI’s New Credit Card Rules: What Changed in April 2026

The RBI has rolled out its most aggressive consumer protection framework to date. Here’s what every Indian cardholder must know:

Mandatory Two-Factor Authentication (Effective April 1, 2026)

Under the RBI’s new Authentication Directions, all credit card transactions — whether online, POS, or contactless — now require at least two independent verification factors, with at least one being dynamic (such as an OTP or biometric scan). This means:

- Static passwords alone are no longer sufficient

- Biometric authentication (fingerprint, face ID) is now a valid second factor

- All banks and payment aggregators must comply — no exceptions

This RBI credit card fraud rule 2026 is a landmark shift that significantly raises the barrier for unauthorized transactions.

Centralized Card Registration System

All active credit cards in India must now be registered in a centralized RBI database. The benefit for consumers: if your card is reported stolen or compromised, it can be instantly deactivated system-wide — preventing fraudulent use even before you file a formal complaint with your bank.

Credit Card Tokenization — Now Mandatory

The RBI’s tokenization mandate requires merchants to replace your actual 16-digit card number with a unique digital “token” for every transaction. This means:

- Your real card number is never stored by merchants

- Even if a merchant’s database is breached, your actual card data remains safe

- Tokenization, credit card, and India RBI compliance are now non-negotiable for all payment processors

New Consumer Rights Under RBI Guidelines for Credit Cards

Per updated RBI guidelines for credit cards, banks must:

- Notify you via SMS/email within seconds of any transaction

- Provide a dedicated 24×7 fraud reporting channel

- Resolve fraud disputes within 90 days (reduced from earlier timelines)

- Offer a minimum zero liability policy for unauthorized transactions reported promptly

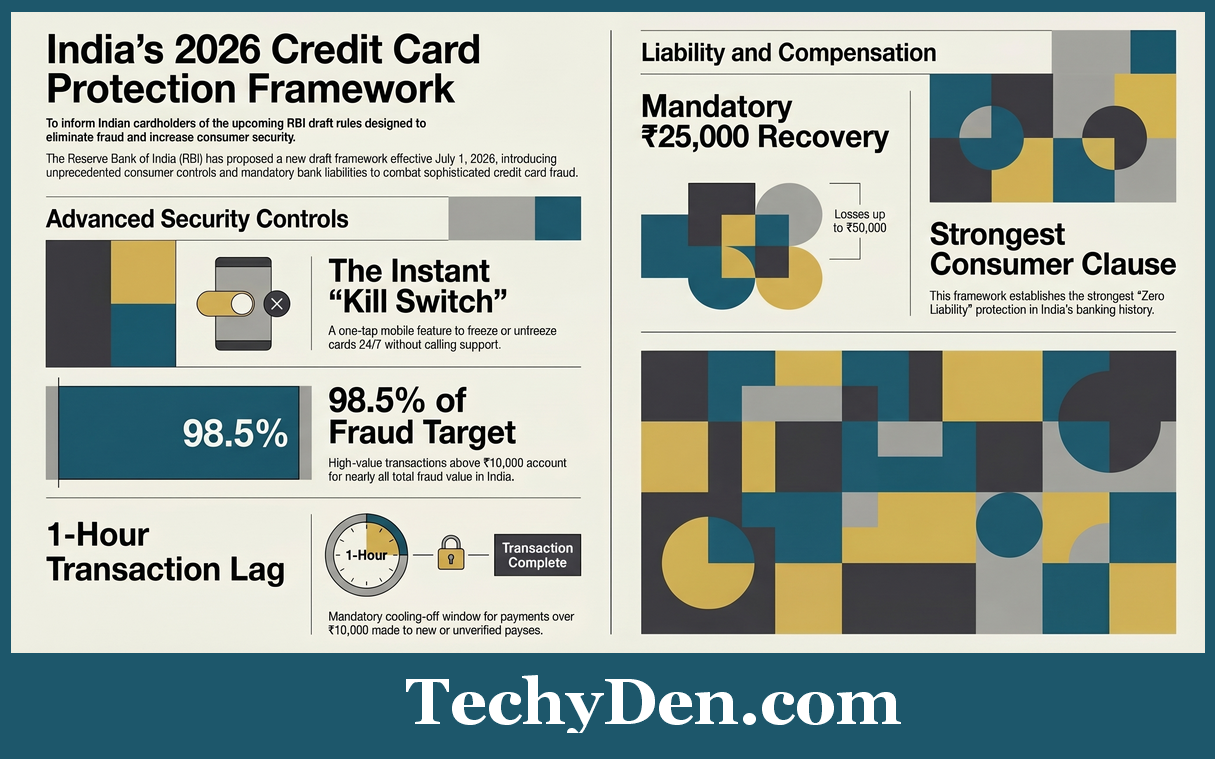

Upcoming RBI Protections: July 2026 Draft Rules

These proposed rules are currently in draft but are expected to be effective July 1, 2026. Publishing and sharing knowledge about these now gives you a significant advantage — most Indian consumers are unaware of these protections.

The Credit Card “Kill Switch”

The RBI is proposing that every Indian cardholder must have access to an instant “kill switch” — a feature in your bank’s mobile app or internet banking portal that lets you freeze your credit card in real time with one tap. No need to call customer service, no waiting on hold.

This is particularly powerful because:

- You can freeze and unfreeze your card instantly during suspicious activity

- Works 24×7, including bank holidays

- Applicable to both physical and virtual credit cards

Lagged Credit for High-Value Transactions

One of the most innovative proposals: a mandatory 1-hour delay on credit card transactions above ₹10,000 to a new or unverified payee.

The rationale is data-driven — transactions above ₹10,000 account for a staggering 98.5% of the total fraud value in India.

This cooling-off window gives both the bank and the cardholder time to flag suspicious activity before money is irreversibly lost.

₹25,000 Compensation for Fraud Victims

Under the draft framework, if you are a victim of unauthorized credit card fraud:

- You are entitled to ₹25,000 compensation for fraud losses up to ₹50,000

- The compensation is mandatory if the fraud is reported within the stipulated window

- Banks that fail to compensate within the prescribed timeline face regulatory penalties

This zero liability credit card India framework is set to be the strongest consumer protection clause in the country’s banking history.

Zero Liability Policy: Your Most Powerful Protection

The zero liability policy means you bear no financial responsibility for unauthorized credit card transactions — provided you report them promptly and have not been negligent with your card details.

How to Claim Zero Liability in India

- Report immediately — Call your bank’s 24×7 fraud helpline the moment you notice an unauthorized transaction

- Send a written complaint within 3 working days (email to the bank’s official fraud reporting address)

- File a cybercrime complaint at cybercrime.gov.in — keep your reference number

- Escalate to the RBI Ombudsman if the bank doesn’t resolve within 30 days

Which Banks Offer Zero Liability in India?

Most major Indian banks — HDFC, SBI, ICICI, Axis, Kotak — offer zero liability protection under RBI guidelines. However, the fine print varies. Key conditions include:

- Fraud must not be caused by your own negligence (e.g., sharing OTP)

- Must be reported within the bank’s stipulated window (typically 3–7 days)

- Applies to card-not-present fraud, skimming, and phishing-related fraud

10 Actionable Credit Card Protection Tips for Indian Users

Here’s exactly how to protect your credit card online and offline — 10 battle-tested credit card security tips India consumers should implement today.

- Never share your OTP, CVV, or PIN — Not with “bank officials,” not with “RBI representatives,” not with anyone. Legitimate institutions never ask for these.

- Enable transaction alerts immediately — Set up SMS and email alerts for every transaction, no matter how small. Fraudsters test stolen cards with micro-transactions (₹1–₹10) before big purchases.

- Use virtual credit cards for online shopping — Many Indian banks (HDFC, Axis, SBI) offer virtual credit card numbers for one-time online use. Even if stolen, they’re useless after the first transaction.

- Activate credit card freeze between uses — With the upcoming RBI kill switch feature, get into the habit of freezing your card when not actively shopping and unfreezing it at the moment of purchase.

- Avoid public Wi-Fi for financial transactions — Public Wi-Fi is a goldmine for man-in-the-middle attacks. Always use a VPN for credit card safety in India or switch to mobile data.

- Regularly check your credit report — Use CIBIL, Experian India, or CRIF High Mark to monitor for unauthorized credit card applications in your name. Free annual credit reports are your legal right.

- Register for 3D Secure (Verified by Visa / Mastercard SecureCode) — This adds an OTP layer specifically for online transactions. Ensure your bank has this enabled.

- Be wary of phishing URLs — Always check that the payment page URL starts with https:// and shows a padlock icon. Fraudulent payment pages often have misspelled bank names (e.g., “hdfcbankindia.net” vs “hdfcbank.com”).

- Protect your card physically — Use RFID-blocking wallets to prevent contactless skimming. Cover the keypad when entering your PIN at ATMs and PoS machines.

- Report SIM-related changes instantly — If your mobile number suddenly loses network for an extended period, call your telecom provider immediately — it could be a SIM swap fraud in progress.

What to Do If You’re a Victim of Credit Card Fraud in India (How to)

Acting within the first few hours dramatically increases your chances of a full refund. Follow this step-by-step process:

Step 1: Block Your Card Immediately

Call your bank’s 24×7 helpline or use the mobile app to block the compromised card. Most banks — HDFC (1800-202-6161), SBI (1800-11-2211), ICICI (1800-1080) — have instant card block options.

Step 2: File a Cybercrime Complaint

Visit cybercrime.gov.in and file a complaint under the “Financial Fraud” category. You can also call the National Cybercrime Helpline: 1930. Keep the complaint reference number for all future communications.

Step 3: Dispute the Transaction With Your Bank

Submit a formal written dispute (email + in-branch) within 3 working days. Attach:

– Your cybercrime complaint number

– Screenshots of suspicious transactions

– Your bank statement shows the fraud

Step 4: Escalate to RBI Banking Ombudsman

If your bank doesn’t respond within 30 days or rejects your claim unfairly, escalate to the RBI Banking Ombudsman at cms.rbi.org.in. The Ombudsman has the authority to award compensation up to ₹20 lakh.

Step 5: Monitor for Identity Theft

After credit card fraud, pull your CIBIL report to ensure no new loans or credit cards were fraudulently opened in your name.

Best Credit Cards in India with Built-In Fraud Protection (2026)

When choosing a credit card, built-in security features are as important as rewards. Here are the key best credit cards with fraud protection in India to evaluate:

| Feature | What to Look For |

|---|---|

| Zero Liability Policy | Full coverage for unauthorized transactions |

| Virtual Card Number | One-time-use card numbers for online shopping |

| Instant Block/Unblock | Via app, no call required |

| Real-Time Alerts | SMS + email + app notifications per transaction |

| EMV Chip + PIN | Superior to magnetic stripe |

| 24×7 Fraud Helpline | Dedicated fraud line, not generic customer care |

| Credit Card Insurance | Optional add-on for fraud loss coverage |

Pro tip for Indians: HDFC Millennia, SBI SimplyCLICK, and Axis Magnus are widely recognized for robust digital fraud protection features in 2026. Always verify zero liability terms before applying.

Credit Card Insurance India: An Extra Layer of Safety

Beyond bank-provided zero liability policies, credit card insurance India plans offer additional protection.

These standalone insurance products (offered by companies like Bajaj Allianz, HDFC Ergo, and Tata AIG) typically cover:

- Unauthorized online transactions

- Card skimming and cloning losses

- Lost/stolen card liability

- Counterfeit card fraud

Premiums are typically ₹500–₹2,000/year — a small price for coverage up to ₹1–5 lakh.

Combine this with cyber insurance for credit card fraud India policies for comprehensive protection, especially if you run a home business or use your card for high-value transactions frequently.

The Technology Fighting Fraud: AI & Tokenization

Indian banks and networks are not fighting fraud passively. Here’s the technology deployed in 2026:

1. AI-Powered Fraud Detection

Banks use machine learning models that analyze hundreds of transaction signals in milliseconds — your spending patterns, location, device, merchant category, and more. An unusual ₹50,000 transaction at 3 AM from an IP in Eastern Europe will trigger an automatic flag and block.

2. Credit Card Tokenization Benefits India 2026

Tokenization replaces your real card number with a dynamic, merchant-specific token. Each token is valid only for that specific merchant and device. Even if a retailer’s database is hacked, the stolen token is worthless anywhere else.

3. Biometric Authentication

With the April 2026 RBI 2FA mandate, fingerprint and face ID authentication are now valid verification methods. This makes stolen card details useless without the physical biometric — a massive leap in credit card security features in 2026.

4. Device Binding

Banks now bind your credit card to specific trusted devices. A login attempt from an unrecognized device triggers immediate additional verification steps, making SIM swap fraud significantly harder to execute.

Frequently Asked Questions (FAQs)

How do I report credit card fraud in India?

Call your bank’s 24×7 helpline immediately, then file a complaint on cybercrime.gov.in or call the National Cybercrime Helpline at 1930. Escalate to the RBI Banking Ombudsman at cms.rbi.org.in if unresolved within 30 days.

What is the zero liability policy on credit cards in India?

Under RBI guidelines for credit cards, if you report an unauthorized transaction promptly and were not negligent (e.g., did not share your OTP), you are entitled to a full refund. The bank bears full liability for third-party fraud.

What are the RBI rules for credit card fraud compensation in 2026?

Under the proposed July 2026 rules, you can receive ₹25,000 mandatory compensation for fraud losses up to ₹50,000, provided the fraud is reported within the prescribed window.

How does the credit card kill switch work in India?

The proposed RBI kill switch is a one-tap feature in your bank’s app to instantly freeze your credit card. It can be reactivated just as easily and works 24×7 without needing to call customer service.

What is credit card tokenization, and how does it benefit me in India?

Tokenization replaces your actual 16-digit card number with a unique digital token for each merchant. Even if that merchant is hacked, your real card details are never exposed — significantly reducing CNP fraud risk.

Is SIM swap fraud common in India?

Yes. SIM swap fraud in India in 2026 is one of the fastest-growing credit card fraud methods. If your phone suddenly loses signal for an extended period, contact your telecom provider immediately and block your credit card.

Can I get credit card insurance separately in India?

Yes. Insurers like Bajaj Allianz, HDFC Ergo, and Tata AIG offer standalone credit card insurance India plans covering skimming, cloning, and unauthorized online transactions at affordable premiums.

What is the difference between authorized and unauthorized credit card transactions in India?

An authorized transaction is one you initiate knowingly. An unauthorized transaction is one made without your consent — whether through fraud, theft, or hacking. Only unauthorized transactions qualify for zero liability protection.

Final Word: Stay One Step Ahead of Fraudsters

Credit card fraud in India is evolving rapidly — but so are your protections.

With the RBI’s landmark April 2026 authentication rules already in effect, and the powerful July 2026 kill switch and compensation framework on the horizon, India is building one of the strongest credit card consumer protection ecosystems in Asia.

Your job is to stay informed, act fast when fraud occurs, and adopt every digital safety hygiene practice available.

Bookmark this guide, share it with family members — especially seniors and first-time cardholders — and check back as the July 2026 RBI rules are officially notified.