In a world increasingly driven by digital payments, virtual credit cards have emerged as one of the smartest tools for safe and seamless online shopping.

Whether you’re a student buying subscriptions, a freelancer paying for SaaS tools, or a business managing ad spend on Google and Meta, virtual cards offer unmatched security without carrying the risks of a physical card.

This guide covers everything you need to know — what virtual credit cards are, how they work, the best options in India for 2026, and why AI-powered virtual cards are changing the game for consumers and businesses alike.

What Is a Virtual Credit Card?

A virtual credit card (VCC) is a digitally generated payment card that comes with a unique 16-digit card number, expiry date, and CVV — but has no physical form.

It is linked to your existing credit or prepaid account and is used exclusively for online transactions.

Think of it as a disposable shield in front of your real card. Even if a merchant’s website is compromised or your virtual card details are leaked, your actual bank account and credit card remain completely untouched.

Unlike a physical card, a virtual card is generated instantly via your bank app or digital wallet, typically accessible only after biometric authentication (fingerprint or face ID) or a PIN.

This makes it not only secure but also extremely fast to deploy for one-time or recurring online payments.

Virtual Card vs Physical Card vs Prepaid Card

Before diving deeper, here’s a quick comparison to understand where virtual credit cards fit:

| Feature | Virtual Credit Card | Physical Credit Card | Prepaid Card |

|---|---|---|---|

| Physical form | No | Yes | Sometimes |

| Instant issuance | Yes | No (5–7 days) | Varies |

| Use case | Online only | Online + Offline | Online + Offline |

| Fraud risk | Very low | Medium | Low |

| KYC required | Minimal to full | Full | Minimal |

| Reload option | Linked to credit limit | N/A | Yes |

| Best for | Secure online shopping | Daily spending | Budgeting |

How Does a Virtual Credit Card Work?

Understanding the working mechanism of a virtual credit card helps you use it more effectively. Here’s the step-by-step process:

- Log in to your bank app or digital wallet (e.g., HDFC NetBanking, ICICI iMobile, or SBI YONO).

- Navigate to the virtual card section and click “Generate Virtual Card.”

- The system generates a unique 16-digit card number, a CVV, and an expiry date linked to your existing credit limit or loaded balance.

- Set a spending limit if the feature is available (HDFC NetSafe and HSBC allow this).

- Use the card details at any online merchant’s payment gateway just like a regular credit card.

- The card expires after the transaction (one-time use) or after a custom period you define.

The key technology powering this process is tokenization. When a virtual card is created, your real card details are replaced with a unique token.

Even if this token is intercepted during a transaction, it cannot be reverse-engineered to reveal your actual account details — making virtual cards nearly impossible to misuse.

AI-Powered Fraud Detection: The 2026 Advantage

One of the most significant upgrades in modern virtual credit cards is the integration of AI and machine learning for real-time fraud detection. This is what truly separates 2026-era virtual cards from their older counterparts.

Modern AI-powered systems use several advanced techniques:

- Anomaly detection algorithms (like Isolation Forest) scan your transaction history and instantly flag any behavior that deviates from your normal patterns — unusual merchant types, abnormal amounts, or unexpected geographic locations.

- Gradient-boosted decision trees (XGBoost) and Graph Neural Networks (GNNs) analyze relationships between transactions, merchants, and devices to detect collusive fraud that single-transaction models miss.

- Visa Advanced Authorization (VAA) and Visa Deep Authorization (VDA) use deep learning to model long-term cardholder behavior, enhancing risk scoring specifically for card-not-present (eCommerce) environments.

- Mastercard’s generative AI algorithms can predict compromised card numbers and block them before criminals even attempt a transaction.

The result? AI systems can detect unusual spending patterns in milliseconds, predict potential fraud before it occurs, and automatically categorize transactions — all without interrupting your checkout experience.

Top Virtual Credit Cards in India 2026

The Indian virtual card market has matured significantly in 2026. With over 900 million internet users and a booming digital payments ecosystem powered by UPI, virtual credit cards have become the go-to tool for secure online spending.

Here’s a detailed breakdown of every major option available right now:

1. HDFC NetSafe — Best Free Virtual Credit Card in India

HDFC NetSafe is the gold standard of free virtual credit cards in India. It has been around for years, but continues to be one of the most trusted and widely used options because of its seamless integration with HDFC’s internet banking ecosystem and zero-cost issuance.

NetSafe works by pulling from your existing HDFC credit card limit — there’s no separate credit check, no new application, and no waiting period.

You simply log in, set the amount, and get a one-time-use virtual card in seconds.

| Feature | Details |

|---|---|

| Network | Visa |

| KYC Requirement | Full (existing HDFC credit cardholders only) |

| Best For | One-time online payments, secure shopping |

| Validity | Single transaction / 24 hours |

| Annual Fee | Nil |

| Spending Limit | Up to your available credit limit |

| Currency Support | INR and international merchants |

How to Generate HDFC NetSafe Card:

- Log in to HDFC Bank NetBanking at netbanking.hdfcbank.com

- Go to Cards → Credit Cards → NetSafe

- Select the credit card you want to link

- Enter the exact amount for the transaction

- A 16-digit virtual card number, CVV, and expiry date are instantly generated

- Use these details at checkout — the card expires after the transaction

Pros:

- Completely free, no hidden charges

- Instant issuance in under 30 seconds

- Linked to existing credit limit — no fund loading required

- Works on all major Indian and international e-commerce sites

- Reduces risk of card skimming and data breaches

Cons:

- Only for existing HDFC credit cardholders

- Single-use only — must regenerate for every purchase

- Not available on the HDFC mobile app (desktop NetBanking only, as of 2026)

- Refunds may take longer since the card expires immediately

Ideal Use Cases: Booking flight tickets on third-party travel sites, shopping on new or unfamiliar international websites, making one-time payments on marketplaces where you don’t want to save your card.

2. SBI Virtual Card (YONO) — Best for SBI Customers

The State Bank of India’s Virtual Card, available through the YONO (You Only Need One) app, is the most accessible virtual card option for India’s largest bank customer base.

With over 500 million SBI account holders, this card has an enormous reach and is trusted by users across Tier 1, Tier 2, and even Tier 3 cities.

What makes the SBI Virtual Card stand out is the custom spending limit feature — you decide exactly how much the card can spend, making it perfect for controlled transactions.

| Feature | Details |

|---|---|

| Network | Visa / Mastercard |

| KYC Requirement | Full (existing SBI account holders) |

| Best For | One-time domestic & international payments |

| Validity | Custom per transaction (typically 48 hours) |

| Annual Fee | Nil |

| Spending Limit | Custom — set at time of generation |

| Currency Support | INR + International |

How to Generate an SBI Virtual Card:

- Log in to the YONO SBI app or SBI NetBanking

- Navigate to Services → Virtual Card

- Choose your linked SBI account or credit card

- Set the spending limit for the transaction

- Copy the generated card number, CVV, and expiry

- Use at checkout — card is valid for the defined period

Pros:

- Available to both SBI debit and credit card holders

- Custom spending limit adds extra financial control

- Accepted at most Indian and international merchants

- Zero fee

- Available via both app and desktop NetBanking

Cons:

- Requires an existing SBI account

- Interface can be slightly less intuitive compared to private bank apps

- Some users report occasional technical delays during high-traffic periods

Ideal Use Cases: Online exam registrations, government portal fee payments, international software subscriptions, hotel bookings, and travel portals where you want strict spending control.

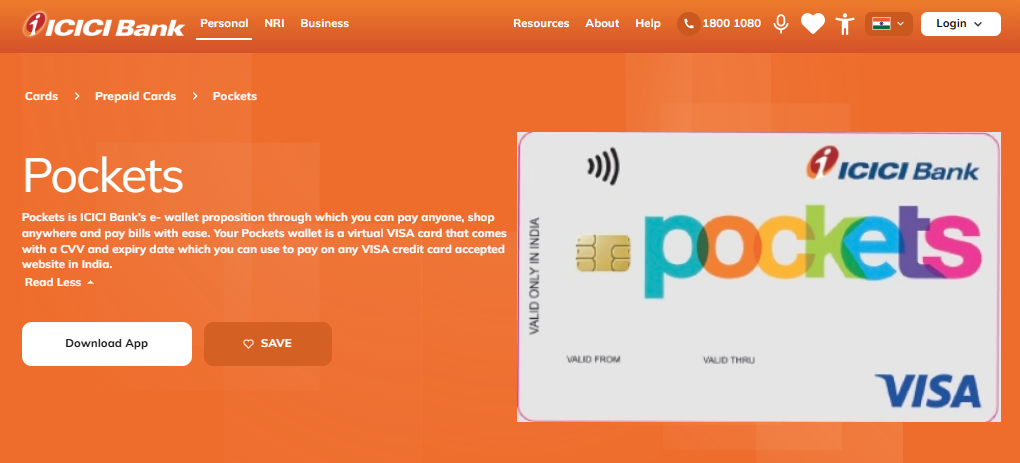

3. ICICI Pockets Virtual Visa Card — Best for Students & Non-ICICI Users

ICICI Pockets is a standout in this list for one key reason: you don’t need an ICICI Bank account to use it.

It is a full-featured digital wallet with a built-in free virtual Visa card, making it one of the most inclusive and accessible options for students, first-time digital payment users, and anyone who wants a virtual card without changing their bank.

| Feature | Details |

|---|---|

| Network | Visa |

| KYC Requirement | Minimal (basic use) / Full KYC (higher limits) |

| Best For | Domestic online shopping, OTT subscriptions, students |

| Validity | Ongoing (until wallet balance is exhausted) |

| Annual Fee | Nil |

| Spending Limit | Up to ₹10,000/month (minimal KYC) |

| Approval Speed | Instant |

How to Get an ICICI Pockets Virtual Visa Card:

- Download the ICICI Pockets app from the Play Store or App Store

- Sign up with your mobile number — no ICICI account needed

- Complete minimal KYC (Aadhaar/PAN optional for basic tier)

- Load money via UPI or net banking

- Navigate to Virtual Card — your Visa card details are generated instantly

- Use the card number, CVV, and expiry at any online checkout

Pros:

- Open to all Indians — no ICICI account required

- Instant card generation with zero fees

- Minimal KYC for basic usage — great for students

- Works on international platforms like Netflix, Spotify, and Amazon Prime

- Biometric app authentication for security

Cons:

- Wallet-based — requires pre-loading funds

- Monthly spending limits are low under minimal KYC

- Full KYC required for higher transaction limits

- Cannot be used at offline merchants or ATMs

Ideal Use Cases: OTT platform subscriptions (Netflix, Amazon, Hotstar), online course payments (Udemy, Coursera), food delivery apps, and first-time online shoppers.

4. Kotak Netc@rd — Best for Subscription & Trial Management

Kotak Mahindra Bank’s Netc@rd is the ultimate tool for anyone who has ever fallen into the trap of a “free trial” auto-converting into a paid subscription.

It allows Kotak credit/debit cardholders to generate single-use or time-limited virtual cards with a maximum cap, making it virtually impossible to be charged beyond what you intended.

| Feature | Details |

|---|---|

| Network | Visa / Mastercard (depends on linked card) |

| KYC Requirement | Full (existing Kotak cardholders) |

| Best For | Subscription management, free trial signups |

| Validity | 24–48 hours or user-defined |

| Annual Fee | Nil |

| Spending Limit | Set manually at generation |

How to Generate Kotak Netc@rd:

- Log in to Kotak Net Banking or the Kotak Mobile Banking App

- Go to Credit Card / Debit Card → Netc@rd

- Select the linked card and set the amount limit

- Define validity period (24 hours, 48 hours, or custom)

- Note down the card number, CVV, and expiry

- Use at checkout — card auto-deactivates after validity expires

Pros:

- Excellent for managing and controlling recurring subscriptions

- Short validity window prevents unauthorized future charges

- Custom spending limits stop overcharging at the source

- Completely free for existing Kotak cardholders

- Easy to generate — takes under one minute

Cons:

- Only for existing Kotak Bank customers

- Very short validity can cause issues with delayed payment confirmations

- Refunds are complex since the card may have already expired by the return date

- Not ideal for repeat purchases at the same merchant

Ideal Use Cases: Signing up for Amazon Prime free trials, Netflix free months, Canva Pro, Adobe Creative Cloud trials, and any software where you want to test before committing to a paid plan.

5. Niyo Global Virtual Card — Best for International Payments from India

For anyone who makes cross-border payments, books international travel, or pays foreign vendors, the Niyo Global Virtual Card is the clear winner in 2026.

Its defining advantage is near-zero forex markup, which saves users thousands of rupees compared to using a standard Indian credit card for international transactions.

| Feature | Details |

|---|---|

| Network | Visa (Global) |

| KYC Requirement | Full KYC (Video KYC available) |

| Best For | International payments, travel bookings, cross-border freelance |

| Validity | Ongoing |

| Annual Fee | Nil (basic tier) |

| Forex Markup | 0% (Zero forex fee on international transactions) |

| Approval Speed | 24 hours |

| Currency Support | 130+ currencies |

How to Get a Niyo Global Card:

- Download the Niyo Global app

- Register with your mobile number and PAN card

- Complete Video KYC — typically approved within 24 hours

- Receive your physical Niyo card by courier (3–5 days) + instant virtual card access

- Load money via NEFT/IMPS/UPI

- Use the virtual card for all international online payments immediately

Pros:

- Zero forex markup — massive savings for frequent international spenders

- Supports 130+ currencies seamlessly

- Excellent for freelancers receiving and spending international payments

- Free international ATM withdrawal (limited per month)

- Pairs well with travel insurance and airport lounge benefits

Cons:

- Full KYC required — not instant for new users

- Physical card takes a few days to arrive (virtual card available sooner)

- Wallet-based (prepaid) — not a credit product

- Some merchants may decline prepaid Visa cards

Ideal Use Cases: Booking international flights on Skyscanner or Expedia, paying for foreign SaaS tools (Ahrefs, SEMrush, Notion, HubSpot), cross-border freelance payments, and traveling abroad without worrying about currency exchange.

6. OmniCard — Best Virtual Card for Students & Teens

OmniCard is a relatively newer but rapidly growing name in India’s virtual card space.

It is specifically designed with students and young adults in mind, offering a low-barrier entry point into digital payments with minimal KYC requirements and a straightforward mobile-first interface.

| Feature | Details |

|---|---|

| Network | RuPay / Mastercard |

| KYC Requirement | Minimal (basic tier) / Full (for higher limits) |

| Best For | Students, teens, low-value online transactions |

| Validity | Ongoing |

| Monthly Limit | ₹10,000 (basic); Higher with full KYC |

| Fee | Small one-time issuance fee |

| Approval Speed | Near-instant |

Pros:

- Low KYC barrier — ideal for students without full income proof

- RuPay support means broad acceptance on Indian platforms

- Simple app interface designed for younger users

- Affordable — issuance fee is negligible

- Can be used on Zomato, Swiggy, Myntra, and major Indian apps

Cons:

- Low spending limit on the basic tier (₹10,000/month)

- Small issuance fee — unlike most bank VCCs, which are free

- International acceptance may be limited on the basic RuPay tier

- Newer brand — fewer user reviews and community support

Ideal Use Cases: Paying for college exam fees, buying books on Amazon India, food delivery, OTT subscriptions, and learning platforms like Unacademy or Vedantu.

7. HSBC Advantage Virtual Card — Best for Granular Spending Control

The HSBC Advantage Virtual Card caters to a more premium segment of users who want complete control over every online transaction.

HSBC’s approach is unique — rather than just setting a single limit at creation, the card allows cardholders to customize limits per purchase category and set advanced transaction rules.

| Feature | Details |

|---|---|

| Network | Visa |

| KYC Requirement | Full (existing HSBC cardholders) |

| Best For | Premium online shopping, granular control |

| Validity | Custom |

| Annual Fee | Nil (for existing cardholders) |

| Spending Limit | Custom per transaction / per merchant |

| Use | Online merchants only |

How to Generate HSBC Advantage Virtual Card:

- Log in to HSBC Online Banking or the HSBC India app

- Navigate to Card Management → Virtual Card

- Set your preferred spending limit and validity window

- Card details are generated — copy or screenshot for use

- Use at any online international or domestic merchant

Pros:

- Highest degree of transaction-level spending customization

- Excellent security — never exposes your real HSBC card details

- Works seamlessly on premium international merchants

- Built on HSBC’s global security and fraud infrastructure

- Biometric and 2FA authentication for access

Cons:

- Not ideal for quick, low-value transactions

- Restricted to existing HSBC credit cardholders

- HSBC has a limited customer base in India compared to SBI or HDFC

- App interface may be less intuitive for first-time users

Ideal Use Cases: Premium hotel reservations on Booking.com or Marriott, luxury shopping on international brands, high-value software purchases, and corporate online expenses where precise budget control is critical.

Quick Comparison: All 7 Virtual Credit Cards

| Card | Network | Fee | KYC | Best For | International? |

|---|---|---|---|---|---|

| HDFC NetSafe | Visa | Free | Full | Secure one-time payments | Yes |

| SBI YONO | Visa/MC | Free | Full | Controlled transactions | Yes |

| ICICI Pockets | Visa | Free | Minimal | Students, subscriptions | Limited |

| Kotak Netc@rd | Visa/MC | Free | Full | Trial & subscription mgmt | Yes |

| Niyo Global | Visa | Free | Full | International payments | Best-in-class |

| OmniCard | RuPay/MC | Small fee | Minimal | Teens, students | Limited |

| HSBC Advantage | Visa | Free | Full | Premium, granular control | Yes |

Best Virtual Credit Card for International Payments

When it comes to a virtual credit card for international payments, you need zero or low forex markup fees and wide acceptance. Here are the top picks:

- Niyo Global — Best for zero forex markup on international spends

- Wise Virtual Card — Excellent for freelancers receiving foreign payments and paying in multiple currencies

- Revolut Virtual Card — Popular globally for travel-related purchases and subscription management

- HDFC NetSafe — Works at most international online merchants with your existing credit limit

If you run a business and need a virtual card for Google Ads, Meta Ads, or TikTok Ads payments, consider Revolut Business or WorldFirst World Card, which are purpose-built for ad platform spending and offer real-time expense tracking across multiple virtual cards simultaneously.

Virtual Credit Cards for Freelancers and Digital Nomads

India’s growing freelancer economy has created a significant demand for virtual debit cards for Indian freelancers.

If you’re a content creator, developer, designer, or digital marketer, a virtual card solves several pain points at once.

Why Freelancers Need Virtual Cards:

- Pay for international SaaS tools (Canva Pro, Ahrefs, SEMrush, Notion) without forex hassles

- Maintain separate virtual cards for each client project to track expenses

- Instantly generate a card for one-time vendor payments without sharing your primary account

- Avoid subscription traps by using single-use cards for free trials

Best Virtual Cards for Freelancers in India:

- Wise Virtual Card — Best for receiving and spending international payments

- Payoneer Virtual Card — Widely accepted, excellent for marketplaces like Upwork, Fiverr, and Amazon

- Fi / Jupiter Virtual Card — Neobank options with zero fees and built-in expense analytics

- RazorpayX Virtual Card — Best for freelancers running a business entity, with automatic GST reconciliation

For digital nomads working across countries, pairing a Niyo Global or Axis Bank Atlas Credit Card with a virtual card adds the dual benefit of lounge access and low-cost international transactions.

Virtual Credit Cards for Businesses and B2B Payments

The business use case for virtual credit cards has exploded in 2026. Companies now use virtual cards to manage vendor payments, employee expenses, ad platform budgets, and SaaS subscriptions — all from a single dashboard.

Key B2B Benefits of Virtual Cards:

- Instant card generation — Issue a new virtual card within minutes for a specific vendor or project

- Custom spending limits — Set per-card or per-transaction limits to prevent overspending

- Real-time expense tracking — Every transaction is logged and categorized automatically

- Automatic reconciliation — Cards like Volopay and Airwallex integrate with accounting tools like Tally, QuickBooks, and Zoho Books

- Multi-currency support — Ideal for paying international vendors without expensive wire transfers

Top Virtual Cards for Businesses in India 2026:

- Volopay — Best for Indian startups needing multi-card, multi-user expense management

- Airwallex — Best for businesses with international payment needs

- RazorpayX — Best for domestic B2B vendor payments with UPI integration

- Standard Chartered Virtual Card — Globally accepted with complete transaction reporting

Using a virtual card for Google Ads payments in particular helps businesses avoid billing disruptions — you can create a dedicated card just for ad spend with a preset monthly limit, ensuring other operations aren’t affected.

Crypto-Funded Virtual Cards: The Emerging Trend

A growing niche in 2026 is crypto-funded virtual credit cards, where users load cards via USDT (TRC20 or ERC20), Bitcoin, or other stablecoins. These are particularly popular among:

- Crypto traders who want to spend without cashing out to fiat

- Cross-border freelancers in regions with limited banking access

- Privacy-conscious users who prefer minimal identity verification

While this category is still emerging in India due to regulatory considerations, global platforms like Wirex, BitPay Card, and Binance Card already offer this functionality. Expect Indian fintech players to introduce regulated versions of this product in the near future.

Who Should Use a Virtual Credit Card?

Virtual credit cards are not just for tech-savvy users. Here’s a breakdown of who benefits most:

| User Type | Why They Need a VCC |

|---|---|

| Online shoppers | Prevent card data theft on less-trusted websites |

| Students | Control spending, pay for international subscriptions |

| Freelancers | Separate business and personal expenses, pay SaaS tools |

| Businesses | Manage vendor payments, ad spend, and team expenses |

| Travelers | Make secure international bookings with low forex fees |

| Privacy-conscious users | Avoid data exposure on new or unfamiliar sites |

Benefits of Virtual Credit Cards

Here’s a consolidated list of why virtual credit cards have become a must-have financial tool in 2026:

- Enhanced security — Tokenization ensures your real card data is never shared with merchants

- AI-powered fraud prevention — Real-time anomaly detection protects every transaction

- Instant issuance — No waiting period; card is ready in seconds

- Custom spending limits — Set transaction-level or monthly spending caps

- Zero physical loss risk — Can’t be stolen, skimmed, or physically misplaced

- Multi-card management — Generate different cards for different merchants, subscriptions, or projects

- Free to use — Most Indian bank VCCs (HDFC, SBI, ICICI, Kotak) are available at zero cost

- Biometric authentication — Modern apps require face ID or fingerprint before displaying card details

Limitations of Virtual Credit Cards

Like any financial product, virtual credit cards have a few limitations to keep in mind:

- Online-only use — Cannot be used at physical POS terminals or ATMs

- Single-use restrictions — Some VCCs expire after one transaction, requiring re-generation for the next purchase

- Not ideal for refunds — Refunds can be tricky if a single-use card has already expired

- KYC barriers — Full-featured cards still require complete KYC, which can take 24+ hours

- Merchant restrictions — Some merchants (especially outside India) may not accept VCCs linked to prepaid wallets

How to Create a Virtual Credit Card: Step-by-Step

Let’s take HDFC NetSafe as an example, since it’s the most widely used free virtual credit card in India:

- Log in to HDFC Bank NetBanking on your desktop or app.

- Go to Cards > Credit Cards > NetSafe.

- Enter the amount you want to transact (this sets the card limit).

- A temporary 16-digit card number, CVV, and expiry date are generated instantly.

- Use these details at your preferred online merchant’s payment page.

- The card automatically expires after the transaction is completed.

For SBI Virtual Card on YONO: Log in → Go to e-Services → Virtual Card → Set limit → Use at checkout.

FAQs About Virtual Credit Cards

Which virtual credit card is best for international payments in India?

Niyo Global and Wise Virtual Card are the best options for international payments — both offer zero or near-zero forex markup and are accepted globally.

Can I use a virtual card on Amazon India?

Yes. All major Indian bank VCCs (HDFC NetSafe, SBI Virtual Card, ICICI Pockets) work seamlessly on Amazon India, Flipkart, and other major e-commerce platforms.

Is a virtual card the same as a prepaid card?

No. A virtual credit card is linked to your existing credit limit and has no physical form. A prepaid card needs to be loaded with funds in advance and may come in physical form.

Can I get a virtual credit card without KYC?

Yes, to a limited extent. Cards like OmniCard and ICICI Pockets offer minimal-KYC tiers with lower spending limits. For higher limits, full KYC is required.

Are virtual credit cards safe for subscription payments?

Absolutely. Using a virtual card — especially single-use or custom-limit cards — for subscriptions is one of the best practices to avoid unwanted recurring charges after a free trial.

Which virtual card is best for Google Ads payments?

Revolut Business and Volopay are purpose-built for ad spend, offering real-time tracking and dedicated virtual cards per ad account.

The Future of Virtual Credit Cards in India

The future of virtual credit cards in India looks extremely promising. With the government’s continued push toward a cashless society, rising UPI adoption, and expanding fintech infrastructure, virtual card usage is set to grow exponentially through 2027 and beyond.

Key trends shaping the future include:

- Deeper AI integration — Predictive fraud prevention, personalized spending insights, and auto-categorization will become standard features

- Wearable and IoT payments — Virtual card tokens will power payments via smartwatches, smart TVs, and even connected vehicles

- Crypto-funded cards — Regulated stablecoin-loaded cards will bridge the gap between crypto holdings and everyday spending

- Embedded finance — Virtual cards will be natively built into e-commerce platforms, freelancing marketplaces, and HR software — no bank app required

- RBI-regulated VCC expansion — Expect more Indian banks and NBFCs to launch feature-rich virtual card products with higher limits and global acceptance

Final Thoughts

Virtual credit cards are no longer a niche tool for the tech-savvy — they are the smart default for anyone who shops, works, or pays online in 2026.

Whether you need a free virtual credit card for online shopping, a secure virtual card for subscriptions, or a virtual card for international payments, there’s an option tailored to your exact needs.

Start with HDFC NetSafe or ICICI Pockets if you’re an individual, move to Niyo Global for international spends, and consider Volopay or RazorpayX if you’re managing business expenses.

The best virtual credit card is the one that fits your spending pattern — and in 2026, you have more choices than ever.